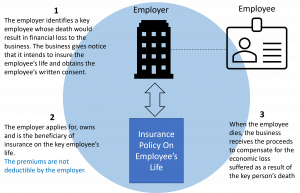

The first life insurance policy in the United States was issued before it was even called the United States.

With centuries to grow and evolve, the life insurance industry now includes hundreds of carriers and thousands of products. So where do you begin?

Life insurance still falls into a relatively small number of categories that can be organized by what you aim to achieve:

- Provide your family with a death benefit if you die before a certain age or before a set number of years have passed

- Provide your family with a death benefit when you die, no matter your age

- Provide your family with a death benefit when you die, no matter your age, and help you save for retirement

By first determining your objectives, you can significantly narrow your search.

Death benefit until a certain age or for a set number of years – Term insurance

Term insurance covers you for a term, either up to a certain birthday or for a fixed number of years. It pays a death benefit only if you die in that term. Term insurance generally offers the largest insurance protection for your premium dollar. If you live longer than that time period (term), then you and your family likely get nothing – unless you have more options. However, those additional options could be considered expensive compared to a standard term policy.

You can renew most term insurance policies for one or more terms even if your health has changed. Each time you renew the policy for a new term, premiums may be higher. Ask what the premiums will be if you continue to renew the policy. Also ask if you will lose the right to renew the policy at some age.

For a higher premium, some companies will give you the right to keep the policy in force for a guaranteed period at the same price each year. At the end of that time, you may need to pass a physical examination to continue coverage, and premiums may increase.

Death benefit when you die – Whole life

Whole life insurance, is a type of permanent insurance, covers you for your lifetime so long as your premiums are paid and your coverage remains in force. You generally pay the same amount in premiums for as long as you live.

Premiums can be several times higher than you would pay initially for the same amount of term insurance. But they are smaller than the premiums you would eventually pay if you were to keep renewing a term policy until your later years.

Some whole life policies let you pay premiums for a shorter period such as 20 years, or until age 65. Most whole life policies do not have any flexibility. You will continue to pay the same premium for the duration of the policy, you cannot adjust the death benefit and there may be no value to you while you are still living.

Death benefit when you die and retirement savings – Universal life

Like whole life, universal life insurance is permanent insurance, but it’s a more flexible type of policy that lets you vary your premium payments. You can also adjust the face amount of your coverage. Increases may require proof that you qualify for the new death benefit.

The other major way universal life varies from whole life is that a universal policy has cash value that can grow as you pay your premiums and be used as an additional tax-advantaged savings vehicle for your retirement. You might see it referred to as cash-value life insurance.

You may borrow against a policy’s cash value by taking a policy loan, using that money for tax-free supplemental retirement income or any other expenses that may come up later in life. If you don’t pay back the loan and the interest on it, the amount you owe will be subtracted from the benefits when you die or will cause your policy to lapse due to insufficient cash value.

Ideally, your premium payments into your policy for the first several years will be enough to not only cover policy expenses, but also create a “cushion” in the policy. This cash value “cushion” will continue to grow based on interest earned so over time you can potentially reduce or stop paying premiums and/or utilize a portion of the cash value as flexible income. It is always important to maintain enough account value in your policy to keep the coverage in force.

Universal life has two common products:

- Fixed indexed universal life (FIUL) – This option allows upside potential if you’re seeking protection and cash value growth. In policies like these, you can place the account value into an “index crediting option” where the growth is tied to market-linked indexes, but your money is never actually invested in the market. That growth can be limited by what’s called participation, cap, and/or spread rates. However, the growth tied to the index are locked in and credited to your account value at the end of each crediting period. Your premium is 100% protected from market losses.

- Variable universal life (VUL) – Unlike an indexed product, your cash value is actually invested in the market (often via mutual funds) and would be subject to the market’s ebbs and flows. Be sure to get the prospectus from the company when buying this kind of policy and STUDY IT CAREFULLY. You will have higher death benefits and cash value if the underlying investments do well. Your benefits and cash value will be lower or may disappear if the investments you chose didn’t do as well as you expected. You may pay extra premium for a guaranteed death benefit.

Best time to buy is when you’re young; next best time is now

Whatever type of insurance is right for you, the sooner you decide, the more affordable your insurance can be. Younger and healthier individuals are less risky to insure, and that means they can get lower premiums – and for some products, lock those lower premiums in for life.

For additional information, you can refer to the Life Insurance Buyer’s Guide, prepared by an independent organization, the National Association of Insurance Commissions (NAIC). Or you can contact your insurance or financial professional.

Don’t have a policy but interested in learning more? Contact us for a no-obligation consultation with a financial professional.